Thai Life Insurance Leaders: Are You Managing Reality or Fantasy?

A candid message for leaders across Thailand’s life insurance industry.

In this latest thought leadership piece, Michael Plaxton challenges business leaders to confront the gap between perception and performance in Thailand’s life insurance market. His message is direct: meaningful progress begins when leaders choose reality over comfort.

A leadership reflection on performance, accountability, and business reality.

In recent weeks, Michael Plaxton has shared a series of insights on distribution, performance, and leadership across Thailand’s life insurance market. This latest article takes a broader view—asking whether business leaders are truly confronting the realities of their organisations, or simply becoming comfortable with underperformance.

It is a challenging read, but an important one. For CEOs, RCEOs, and senior distribution leaders, the message is clear: real improvement starts with honest self-assessment, disciplined execution, and the willingness to confront difficult truths.

Do you live in a World where you can separate what is real from what is from illusion? Or do

you prefer existing in a state of “make believe”?

Unfortunately today some leaders live in the fantasy World where thing appear to be better

than they really are! Some examples:

1) The leader who believes they have all the answers to the business challenges. But the reality is that nobody does so “kill the ego” and engage your whole team on solving the problem.

2) The Leader who believes that winning wards should make my Board happy regardless of whether we hit the year’s plan or not! An award might make you feel good but only results will keep all your Stakeholders satisfied.

3) Then there is the leader who willingly and knowingly creates the illusion of success when they are simply delaying the day that reality hits everyone!

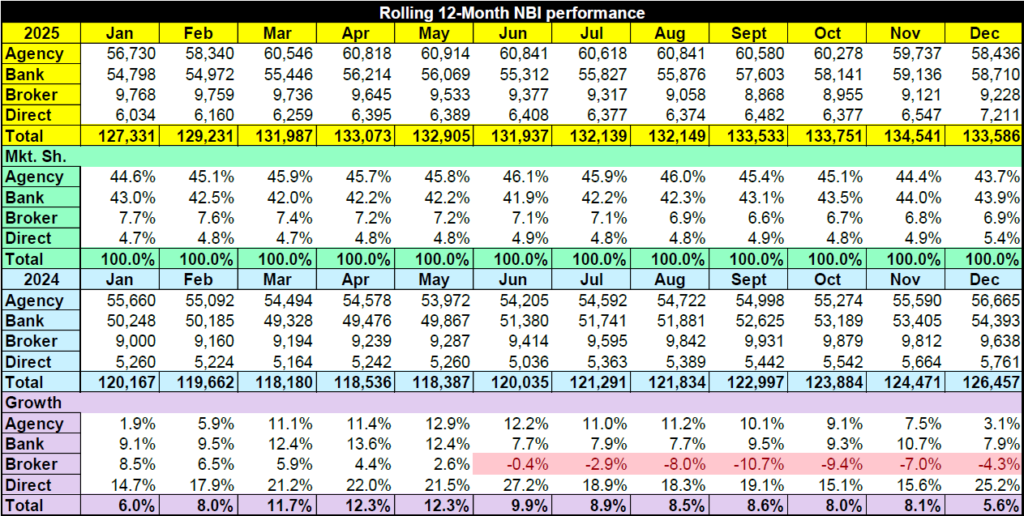

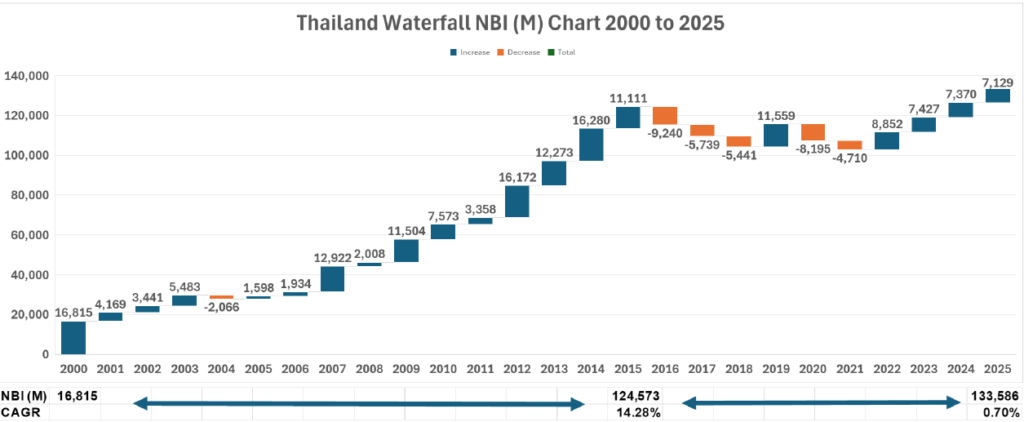

When I was reviewing the Industry results for the Thai Life Insurance Market for the full year

2025 I was struck by the question – is the result real? Why did I think of that question?

The numbers show Industry growth of new sales (NBI) at 5.6% year-on-year. Whilst this is no where near the Halcyon days when Thailand was an “Asian Tiger” with surging growth it is a strong result for recent years.

Should we take the numbers at face value and move on or should we look deeper? I like to deal with reality, so I looked at the numbers for the year in more detail.

Challenges:

1) The Health Rider “Fire Sale” in Q1. The OIC introduced new rules around claims for

Health Insurance to encourage Customers to take more responsibility in the process.

This delivered an increase of Bt. 3.8 billion but remember it is a Rider and so would

increase the base plan sales to which it was attached for a total of at least Bt. 7.5 billion.

2) At least 3 companies offered very short-term Endowment Savings Plans. Together

they probably added Bt. 2 billion questionable sales to total sales.

3) Year-end push to close on a high. December is always a strong month often for good

reasons such as bonus earnings of distributor partners or Banks closing their financial

year looking to maximize results. The Digital Direct channel has struggled to justify the

investment made over the last few years. This year one company offered a short-term

savings plan plus merchandise and delivered results at least Bt. 0.5 billion over the

previous year’s result.

4) Our company is a champion of the customer. We grow Financial Planners – career

agents who provide a valuable service to our customers. All designed to build customer

loyalty.

5) Our company leads the Health Market. In truth only one company can say that, and

they deliver 51% of all health sales. Those that claim to lead have a share of between

1% and 6% which is by no means leading the market!

If we deduct these “illusions” we find that the market did not grow. But even that

conclusion would be “smoke and mirrors”! Why? Simply because similar things

happened in previous years – perhaps not as significantly but for sure 2024 would have

some questionable numbers.

Why does it matter?

We move on without recognizing the “Monsters” we have created!

Some, but not all, of the Health “Fire Sale” raise concerns about misselling. “The old plan is

cheaper!” The old plan’s “claims are old basis!” Neither is it necessarily true. The new regulations will apply to all claims whether the policy is new or old. The challenge will be that

the new rules are more complicated for the customer to understand and put the Insurance

Company in charge of the claims finally paid.

When customers are uncertain and even confused it leads to some turning to litigation to

solve the problem. Have you built a plan for potential future litigation?

The short-term Savings plans create financial problems. In a couple of cases these plans

offer food customer returns, mature in just 3 years with only 2 years’ payments. The 2 years

allows it to rank as annual premium! The problem is they have low, potentially negative

margins, and create IFRS17 issues around accounting for the liability. Significant volumes

will stress future Total Premium (a key top line financial contributor) – within 2 years there

are no more premiums to collect and so the company will need to find a replacement! Do

you have a plan for these contingencies?

The false numbers in the Digital Direct Channel will encourage everyone to repeat the

exercise to justify the investment made. The problem is the result is not real. This channel

is not unlike the old Direct Mail efforts of 30 years ago. DM was also going to be the channel

of the future. They also cut margins to a minimum. They also offered merchandising to

encourage the customer to buy. Today we see the results – from the DM investment. Early

lapses, unhappy customers that don’t trust us, and warehouses full of returned merchandise!

How solid is your Digital Direct Channel strategy (and execution)?

The last 2 examples I raised of “smoke and mirrors” are about making announcements on

which we are clearly not delivering. It leads to distrust by customers which in turn leads to

premium payments being stopped. How do you monitor and manage unhappy

customers?

We move on without fixing the underlying business issues!

Agency

In Thailand, the Agency channel is predominantly Part-Time. Sure there are some full-time

workers, but their numbers are small. Consider the table below:

Agent numbers are falling as other career opportunities have appeal. With case productivity

of only 0.6 per agent per month we MUST conclude that agents are mainly part-time. Simply

put only 60% of agents write one case in any month. It is just not enough to put food on the

table for the family. It has been at this poor level since my first memories of Thailand in 1995

when productivity was just over 0.5 cases.

Companies must change their approach and strategy for Agency growth:

1) Improve recruitment processes including how to say no to an unsuitable candidate.

2) Improve the onboarding process and give them a vision of delivering a quality service to

customers based on the CUSTOMER’S PRIORITIES based on their life journey and

family responsibilities.

3) TRAIN THEM FROM DAY ONE TO BE FULL-TIME FINANCIAL PLANNERS.

4) Build a career plan around the Agent’s aspirations that cover the money they want to

make not the numbers required by the company.

5) Manage them to be active every day – prospecting by network building, approaching for

meetings, presenting solutions based on a full need analysis, giving the customer a

solution they can afford and providing regular after-sales service to ensure satisfaction.

6) Motivate them with compensation that rewards productivity AND SALES QUALITY.

7) MORE TRAINING TO COPE WITH ANY ASPIRATIONS REGARDING BUILDING

STRONGER SALES EXPERTISE AND/OR PREPARING THEM FOR A

MANAGEMENT ROLE.

8) Regular ongoing personal development coaching from the manager.

9) Document the whole process – use the agents’ personal data to identify development

needs.

The hard truth about the data is that it tells us that ZERO Companies in Thailand that are

delivering this full strategy – nobody has an agency productivity exceeding a case per month.

Professional Agents would deliver 4 cases per agents per month or more!

When the Agent wins so does the insurance company. WE ARE IN IT TOGETHER.

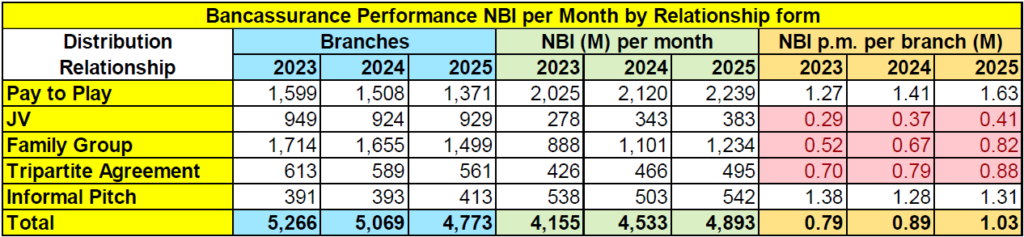

Bancassurance

In Thailand there are many Bancassurance models of varying success.

The “Pay-to-Play” relationship between the Bank and the Insurance Company seems to offer

the most productive results. So let’s understand the strategies employed by these

companies that, executed well, deliver superior results.

1) Both parties want success by negotiated agreement – they understand what it looks like!

They share a vision which is about improving the lives of the Bank’s customers. The

same conclusion is reached by those companies competing in the “Informal Pitch” hence

the good results they deliver.

2) Both parties work on the business plan together. Not simply the numbers each needs to

justify the arrangement each year but also the actions each party with undertake to

execute.

3) Both parties meet every month to review progress and agree to changes in the actions

needed for success.

4) Products are developed together. The Bank understands the Customer’s needs better

from the relationship they have with each customer. The Insurance Company

understands how to build product solutions that best meet the customer’s needs.

5) The Sales and Marketing plan is a shared responsibility:

a) Whilst it is great when the Bank’s head office has specific plans and activities

planned for the year to encourage sales they have Bank products to promote as well.

So strong productive relationships need to be built at high level in both organizations

for delivering the best results.

b) As mentioned earlier the Bank has other products to sell and so the Insurance

Company must provide local sales and marketing support at branch level to deliver

a consistent coordinated approach to meeting the share of vision for the customer.

6) Training and Licensing is the responsibility of the Insurance Company. This is supported

by local coaching at Branch level.

7) Compliance and Complaints are joint responsibilities which should be coordinated

through monthly meetings of the two teams.

8) Compensation is important to be agreed. Whilst few Banks directly reward sellers with a

share of the fees earned (best results is when they do) the Insurance Company should

help to build a relevant requirement into the “Score Card” appraisal system used by

many Banks to make annual bonus payments.

9) Jointly automate the whole process. Banks are understandably protective of their IT

systems, but it should still be possible to build tools to help – prospecting, need analysis,

preparing illustrations of products, virtual applications, some level of virtual underwriting,

gathering the premiums, etc.

When the Bank wins so does the Insurance Company. WE ARE IN IT TOGETHER.

Broker

Brokers are often seen as a provider that can solve an Insurance Company’s weak top-line

results through acquiring large Group EB which is wrongly seen as the only avenue for

such products.

The table clearly shows that Brokers can sell other lines of business and we will show later

that Group EB can come from other Channels. There is a Golden Opportunity with Brokers.

Help them to build a business plan through support from the Insurance Company that allows

them to consolidate their Corporate and Individual Customers into a more comprehensive

business plan:

1) Have a shared vision with each Broker about their Customers (Corporate and Individual)

and the future of the Broker’s enterprise.

2) Build a plan together to exploit the customer base of the Broker:

a) Yes, look for Group EB but make sure you can improve the poor Renewal risk

associated with this business. Brokers have to move it every 3 or 4 years to protect

their large Corporations from competing Brokers – as I have mentioned many times

before. Solutions include:

i) Seek sharp rates through log-term agreements with the Customer. Offer to handle member questions, claims, etc. through direct service of those members.

ii) Make the technology used for this member helpline open to the Broker and the

Corporation so they can track what is happening.

iii) This process saves both the Corporation and the Broker time and money.

iv) The Insurance Company gets online access to the Membership for potential

Direct Digital sales later.

b) Corporations have Owners and many high-net-worth executives who need personal

advice for Estate Protection, Estate Tax Planning, Key Employee Protection, Golden

Handcuffs, and a whole load of other products.

c) Corporations have many employees and they often go to their employer for financial

advice (usually financial assistance). Talk to Corporations about offering “Worksite

Marketing” to encourage employees to make themselves more financially

independent.

d) Build a sales team in the Brokers business to market life insurance directly to the

motor, household, and other non-life insurance customers. Take responsibility for

licensing and training.

e) Build a Digital platform to sell life products.

f) So far only a few companies have worked to expand the Brokers business. But the

potential is much greater and needs a complete strategy to deliver it.

When the Broker wins so does the Insurance Company. WE ARE IN IT TOGETHER.

Direct to Customer

This comprises of 4 subchannels but it seems that the one everyone promotes is Digital

Direct! Big mistake if that includes you.

First let me remind you that around 750 million of the November and December sales is

“smoke and mirrors”. Hence Digital Direct is well overstated. But even with these inflated

numbers Face-to-Face Direct Sales and Telemarketing are delivering higher sales and from

a much lower expense base!

Thoughts:

Digital has questionable sales in November and December (you can probably halve the

Endowment and Health premiums).

Direct Mail is a dead channel, but when you look at renewal history all you see are lapses!

Is this a possible outcome for Digital which is also seen as the future channel of self-

determining customers!

F2FDS has regular sales every month. It seems some Corporations prefer dealing directly

for their Group EB! And if you get then as your customers you have all the options outlined

for the Brokers – marketing HNW plans, solutions to make employees financially

independent through worksite marketing, and Digital Direct from the database of members.

Telemarketing also has a great track record of sales. It does have challenges in weaker

Renewals, but these can be addressed.

When the Customer wins so does the Insurance Company. WE ARE IN IT TOGETHER.

Conclusions.

1) Blow away the “smoke and mirrors.” Let the data talk to you about what is really happening in your business.

2) Build more comprehensive strategies for every channel. There is so much potential when you see the realities.

3) No one person has all the answers. Kill the EGO, share the thoughts and the data with your whole team. Listen to all the ideas. Evaluate all the ideas – theirs as well as your own. Make sound choices – build the plan together.

Credit : Mike Plaxton – March 11, 2026

This article is part of Michael Plaxton’s ongoing thought leadership series examining leadership, performance, and distribution effectiveness in Thailand’s life insurance sector.

We invite industry leaders and professionals to reflect on these perspectives and continue the conversation.

Written : Michael Plaxton

Independent consultant.

Former CEO of FWD Thailand, former CEO of Krungthai-AXA Life Insurance.

This is a Money Playschool x Michael Plaxton collaboration. Find the original article here

![Private: [ID: 1uCGuYuY8nc] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/04/29110005/private-id-1ucguyuy8nc-youtube-a-60x60.jpg)

![Private: [ID: DwjgyvoWpUk] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/06/08110004/private-id-dwjgyvowpuk-youtube-a-236x133.jpg)

![Private: [ID: ymQlCqFlMDs] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/06/05110005/private-id-ymqlcqflmds-youtube-a-236x133.jpg)

![Private: [ID: PeI-SwJQ4Fg] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/06/04110005/private-id-pei-swjq4fg-youtube-a-236x133.jpg)

![Private: [ID: 1uCGuYuY8nc] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/04/29110005/private-id-1ucguyuy8nc-youtube-a-236x133.jpg)

![Private: [ID: R6MEEAr-Ffo] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/04/28110004/private-id-r6meear-ffo-youtube-a-236x133.jpg)

![Private: [ID: eTGxlhp8dD0] Youtube Automatic](https://images.moneyplayschool.com/uploads/2026/04/27110005/private-id-etgxlhp8dd0-youtube-a-236x133.jpg)